Executive Summary

~2 min listen

~38 min read

~38 min read

The Bottom Line

A February 21, 2025 White House memorandum weaponized Section 301 tariffs against foreign digital services taxes — covering 16 countries and ~$370 billion in Chinese imports — meaning tech founders with revenue in France, UK, India, or Turkey must restructure their IP before USTR determinations lock in new tariff rates.

Value of Chinese imports currently subject to Section 301 tariffs.

Annual U.S. economic cost of IP theft, majority attributed to China.

Turkey's Digital Services Tax rate — the highest among countries under U.S. scrutiny.

What You Need to Know

Section 301 is uniquely dangerous for trading partners because it requires no injury finding and no WTO exhaustion — the USTR can initiate tariffs within 12 months of opening an investigation. The 2024 four-year review proved it's not a sunset mechanism: EV tariffs jumped from 25% to 100% and semiconductor tariffs were set to hit 50%, showing tariffs can escalate as easily as they can expire.

The 2025 White House directive formally equates discriminatory digital taxation with forced technology transfer — the same legal theory that justified $370 billion in China tariffs now applies to France's 3% DST and Turkey's 7.5% gross-revenue levy. Because DSTs tax gross revenue rather than profit, U.S. platforms pay regardless of margins, and threshold structures are calibrated to hit American companies while exempting smaller European and Asian competitors.

What To Do Next

Audit your IP ownership structure to identify assets exposed to DST jurisdictions before USTR determinations finalize.

Submit public comments during the USTR's Federal Register notice period to document your company's specific economic exposure.

Review all China-adjacent joint venture or licensing agreements for forced technology transfer risk and minimize proprietary disclosures.

Monitor the October 2025 Section 301 investigations into 16 countries for tariff rate announcements affecting your supply chain or revenue markets.

Consult an IP attorney to restructure licensing and revenue allocation in France, UK, Italy, Turkey, and India before new tariff rates take effect.

Jump to Section

Why Section 301 is America's fastest and most powerful trade weapon

How China's IP extraction system triggered $370B in tariffs

The 2025 memo that made digital taxes a tariff target

Exactly which products and rates face Section 301 tariffs today

What Section 301 means for your tech company's IP strategy

Concrete next steps to protect your business from tariff exposure

0:00

Foreign governments collected billions of dollars from American technology companies last year through taxes and regulatory structures specifically designed to capture revenue from U.S. platforms and a February 21, 2025 White House memorandum called it exactly what it is: plunder. The administration's chosen weapon to fight back is Section 301 tariffs, a statute that has been quietly reshaping global trade since the Trade Act of 1974 was signed into law. For tech founders and IP holders, what happens under Section 301 of the Trade Act of 1974 is not abstract trade policy it is the mechanism that determines whether the intellectual property your company spent years building gets protected or systematically extracted by foreign governments and their state-backed competitors.

What Section 301 of the Trade Act of 1974 Actually Does and Why It Matters Now

Section 301 of the Trade Act of 1974 is not a tariff schedule it is a statutory grant of power. It authorizes the U.S. government to investigate foreign government behavior and impose economic consequences when that behavior systematically harms American businesses. The China Section 301 action that began in 2018 now covers approximately $370 billion in imports. The 2025 White House memorandum extended the statute's reach to digital services taxes targeting U.S. technology companies. Understanding what the law actually does and what makes it different from every other U.S. trade statute is the necessary foundation for understanding why it became the administration's instrument of choice for protecting American IP.

The Statutory Foundation That Gives the U.S. Government Its Most Powerful Trade Weapon

Section 301 of the Trade Act of 1974, codified at 19 U.S.C. § 2411, grants the U.S. Trade Representative (USTR) authority to investigate foreign government practices that are "unreasonable," "unjustifiable," or "discriminatory" when those practices burden or restrict U.S. commerce. The statute does not require the government to prove economic injury through a quasi-judicial proceeding before acting, a structural feature that makes it qualitatively different from most other trade remedy statutes and considerably faster.

The law was designed with a specific type of adversary in mind: foreign governments that use regulatory, tax, or market-access structures to systematically disadvantage American businesses rather than individual importers or exporters engaged in conventional dumping. According to the Congressional Research Service, a Section 301 investigation can be self-initiated by the USTR or triggered by a petition from an affected industry, and the process begins with a Federal Register notice inviting public comment, followed by public hearings and formal consultations with the foreign government. The USTR aims to reach a determination within 12 months when no trade agreement is involved.

The trade act of 1974 Section 301 distinguishes between "mandatory" action cases where a trade agreement right has been denied or an "unjustifiable" practice has been identified and "discretionary" action, where the USTR has latitude to determine whether the practice warrants retaliation. Digital Services Taxes and forced technology transfer sit in the "unreasonable or discriminatory" category, which gives the executive branch significant flexibility in timing and scope. The breadth of available remedies under the Section 301 trade act 1974 runs from targeted tariffs to broad import restrictions, making it the most versatile weapon in the U.S. trade arsenal.

The Federal Register notice requirement matters to businesses beyond its procedural role: it opens a formal public comment period that affected companies can and should participate in. A company whose supply chain, licensing structure, or market access is affected by the foreign practice under investigation has standing to submit comments and those comments become part of the administrative record that shapes USTR's determination. For technology founders building IP-intensive businesses, this participation right is an underused strategic tool. Resources like the AI Patent Mastery guide can help frame how your innovations fit into the broader IP protection landscape that Section 301 is designed to defend.

How Section 301 Differs From Every Other U.S. Trade Statute in Scope and Speed

The United States maintains several trade remedy statutes, and the differences between them are not academic they determine which mechanism fits which type of trade dispute. Section 232 of the Trade Expansion Act of 1962 authorizes tariffs on national security grounds but requires a formal investigation by the Department of Defense and Commerce, a finding that imports threaten national security, and presidential action. Section 301 of the Trade Act of 1974 provides "safeguard" protection for domestic industries injured by import surges, but it requires an injury determination by the U.S. International Trade Commission. Antidumping and countervailing duty laws address specific unfair pricing and subsidy practices for specific imported goods, requiring detailed cost calculations and administrative determinations.

Section 301 requires none of these predicate findings. The USTR can initiate an investigation based on a determination that a foreign government practice is "unreasonable" and initiate tariff action within 12 months. According to the Congressional Research Service, between 1995 and 2017, Section 301 was used sparingly mostly to pursue WTO dispute cases rather than unilateral action. The Trump administration's first term changed that, initiating multiple Section 301 investigations and generating two major sets of tariffs: the China IP action and an action against EU subsidies for Airbus.

Section 301 requires none of these predicate findings. The USTR can initiate an investigation based on a determination that a foreign government practice is "unreasonable" and initiate tariff action within 12 months. According to the Congressional Research Service, between 1995 and 2017, Section 301 was used sparingly mostly to pursue WTO dispute cases rather than unilateral action. The Trump administration's first term changed that, initiating multiple Section 301 investigations and generating two major sets of tariffs: the China IP action and an action against EU subsidies for Airbus.

The structural flexibility is exactly why the White House chose Section 301 tariffs to respond to Digital Services Taxes and China's forced technology transfer china practices. When the offense is a foreign government's IP extraction policy or discriminatory tax structure rather than a specific imported product being dumped at below-market prices, Section 301 is the only statute that targets foreign government behavior directly rather than specific goods crossing the border. The other statutes require you to identify the product. The section 301 trade act 1974 lets you target the policy itself, including unfair trade practices that no product-specific statute could reach.

Section 301 also has a different relationship to World Trade Organization dispute resolution than other statutes. The USTR can pursue Section 301 actions unilaterally without first exhausting WTO remedies when urgency warrants it, a critical advantage given that World Trade Organization dispute settlement typically takes three to five years from panel establishment to final appellate ruling.

The Four-Year Statutory Review Requirement and What the 2024 Review Revealed

Section 301 includes a built-in accountability mechanism: under 19 U.S.C. § 2417, the USTR must conduct a review of any tariff actions no later than four years after they are imposed to determine whether they are achieving their objectives and whether continuation, modification, or termination is appropriate. The 2024 four-year review of the China Section 301 tariffs was the most significant such review in the statute's history.

According to AP News, the Biden administration's May 2024 determination not only continued the tariffs but increased them substantially across strategic sectors. Electric vehicle tariffs rose from 25% to 100% (bringing total combined duty to 102.5% when standard MFN rates are included). Solar cell tariffs increased from 25% to 50%. Semiconductor tariffs were set to increase to 50% by 2025. Lithium-ion EV battery tariffs were scheduled to rise from 7.5% to 25% by 2024 and further by 2026. The review received hundreds of public comments from industry, labor organizations, and trading partners.

The criteria applied in the review reveal what "achieving their objectives" means in practice: the USTR examines whether the foreign government has modified or eliminated the unfair practices identified in the original investigation, whether the tariffs have created economic distortions that outweigh their benefits, and whether continuation serves the broader national economic interest. The 2024 findings concluded that China had not meaningfully reformed its IP and technology transfer practices which are the same practices that originally triggered the original investigation remained substantially in place and that the tariffs therefore remained warranted.

The practical implication for businesses is that the four-year review is not a sunset mechanism. It is a calibration opportunity, and the 2024 results demonstrate that Section 301 tariffs can increase as well as decrease. Any business importing from China should treat the next review cycle as a live compliance event requiring ongoing monitoring, not a fixed endpoint.

How China's Forced Technology Transfer Practices Triggered the Largest Section 301 Action in History

The 2018 USTR Section 301 investigation into China was not about conventional tariff disparities or dumped goods. It was about a systematic government policy of intellectual property extraction which is a policy architecture designed to transfer proprietary technology from foreign companies to Chinese domestic competitors as the price of market access. For tech founders and SaaS companies whose IP is their core asset, understanding how that system operates is essential context for understanding both the tariff regime and their own exposure. The SaaS Patent Guide 2.0 provides additional context on how SaaS founders can structure IP protection in this environment.

What Forced Technology Transfer Actually Means and How China's System Operationalizes It

Forced technology transfer is not a single policy. It is a system of interlocking requirements, informal pressures, and market access conditions that collectively compel foreign companies to surrender intellectual property in exchange for the right to operate in China. The mechanisms are structural, not incidental.

The most visible mechanism is the joint venture requirement. According to the Congressional Research Service, from 1994 until 2018, China required foreign automakers to form joint ventures with Chinese firms capped at 50% foreign ownership giving the Chinese partner legal access to proprietary manufacturing technology, engineering processes, and supply chain data. The automotive sector is the clearest example, but analogous joint venture requirements applied across manufacturing, technology, and financial services sectors.

Beyond joint ventures, Chinese regulations restrict royalty rates in technology licensing agreements between foreign IP owners and Chinese licensees, effectively setting below-market price ceilings on U.S. intellectual property. Administrative licensing processes for market entry require disclosure of trade secrets as a precondition for regulatory approval. State-backed acquisitions of U.S. technology companies, coordinated through Chinese government industrial policy programs, provide another channel for acquiring foreign technology with state resources rather than commercial transaction value. These forced technology transfer china mechanisms work in concert, making it difficult for any foreign company to enter the Chinese market without surrendering some degree of proprietary control.

The USTR's 2018 Section 301 investigation documented all of these mechanisms explicitly. The resulting report, approximately 182 pages, found that China's practices were "unreasonable" within the meaning of 19 U.S.C. § 2411(b)(1) because they burdened and restricted U.S. commerce through a coordinated government policy rather than legitimate regulatory activity. The Section 301 tariffs on approximately $370 billion in Chinese goods were the statutory remedy for that documented, quantified harm.

For a U.S. technology company considering any commercial arrangement involving a Chinese partner, government entity, or market access application, the operational implication is direct: any proprietary technology disclosed in that context may be treated as accessible to the Chinese partner under Chinese regulatory frameworks. IP protections must be structured before entering those arrangements, not retrofitted afterward. Protecting IP begins with documentation, the Patent Documentation Blueprint outlines how to build the kind of legally defensible record that supports both patent prosecution and trade secret protection in high-risk commercial environments.

The China State Capitalist Model and Why It Makes Standard IP Protections Insufficient

China's approach to technology transfer is not a market failure, it is a feature of a state capitalist system in which the government actively coordinates corporate behavior toward national industrial policy objectives. This distinction matters enormously for U.S. technology companies because it means standard commercial IP protections are structurally insufficient in the Chinese market context.

Under this model, Chinese courts, regulators, and state-owned enterprises function as coordinated instruments of industrial strategy. The USTR's 2018 report characterized the practices as "systematic" and documented the role of Chinese government instrumentalities in directing and facilitating technology acquisition from foreign firms. A foreign company's trade secret is not just at risk from a dishonest business partner as it may face administrative demands from Chinese government entities, transfer to state-owned competitors through opaque regulatory processes, or appropriation through cyber espionage linked to state actors. This is the core reason why forced technology transfer china presents a categorically different risk than IP disputes in Western commercial environments.

According to AP News, the FBI Director has stated that China has a larger hacking program than every other nation combined, aimed specifically at stealing sensitive data and trade secrets from U.S. companies. Former NSA Director Keith Alexander described Chinese state-directed IP theft as "the greatest transfer of wealth in history." The IP Commission Report estimated that IP theft, the majority of it attributed to China, costs the U.S. economy between $225 billion and $600 billion annually, and that approximately 87% of counterfeit goods seized at U.S. borders originate from China.

The downstream economic consequence of this technology acquisition model is structural excess capacity driven, in significant part, by forced labor and forced labor import restrictions that U.S. law imposes on goods produced under such conditions in manufacturing supply chains. Chinese domestic producers gain access to foreign technology without bearing the R&D cost, and in many sectors benefit from labor cost structures that include state-directed prison or coerced labor, allowing them to undercut on price and flood global markets. According to AP News, state-subsidized Chinese electric vehicles can sell for as little as $12,000, and China's solar panel and steel output is so large it could supply much of global demand at prices that effectively eliminate foreign competition. The Section 301 tariffs are, at least in part, a response to this downstream effect is an attempt to price back into the market the R&D costs that Chinese producers avoided through forced technology transfer and the labor cost distortions created by forced labor in certain manufacturing sectors.

For U.S. technology companies, the implication is that protecting IP in any China-adjacent commercial context requires a framework that assumes state involvement in any enforcement environment and that minimizes disclosure to the absolute minimum required for the legitimate business purpose.

How the USTR Quantified the IP Harm and Built the Legal Case for Section 301 Action

The 2018 USTR Section 301 investigation into China was the largest and most consequential in the statute's history. It was initiated in August 2017, invoking the trade act of 1974 Section 301, specifically targeting China's practices related to technology transfer, intellectual property, and innovation is not a conventional tariff, dumping, or additional tariffs complaints. The investigation lasted approximately seven months and produced a report of approximately 182 pages documenting specific practices, their legal basis in Chinese law, and their economic impact including harm to intellectual property rights on U.S. companies.

The USTR made four core findings. First, China uses foreign ownership restrictions and joint venture requirements to force technology transfer as a precondition for market access. Second, China directs and facilitates the acquisition of U.S. companies and assets to obtain cutting-edge technologies, often through state-managed investment vehicles. Third, China conducts or supports cyber intrusions into U.S. commercial and government networks to steal technology and trade secrets. Fourth, China directs companies to acquire technology pursuant to industrial policy plans, particularly the "Made in China 2025" strategy targeting ten strategic technology sectors. Each finding mapped to the "unreasonable" or "discriminatory" standard in the Section 301 trade act 1974, constituting a formal legal determination that China's conduct warranted remedial action.

The tariff response was structured in escalating tranches, with each tranche generating federal revenue while imposing costs on Chinese export industries. List 1 ($34 billion, imposed July 2018) targeted industrial machinery, aerospace parts, and technology components specifically chosen to impose maximum pressure on China's "Made in China 2025" objectives. List 2 ($16 billion, August 2018) added semiconductors, plastics, chemicals, and railroad equipment at 25%. List 3 ($200 billion, September 2018) broadened the scope dramatically to consumer electronics components, networking equipment, and hundreds of other categories at an initial 10%, later raised to 25%. According to the Congressional Research Service, the total value of imports subject to section 301 tariffs reached approximately $370 billion covering the vast majority of Chinese imports into the United States.

The critical point for understanding the tariff regime's durability is that the USTR built the China Section 301 tariffs case on documented, systematic government behavior. The tariffs are not a response to a specific trade dispute or a particular product's competitive advantage. They are the statutory remedy for a documented government policy of IP extraction. That evidentiary foundation is why the Section 301 tariffs survived the transition from the Trump to the Biden administration and back, and why multiple four-year reviews have resulted in extension rather than termination.

The February 2025 White House Directive That Expanded Section 301 to Digital Services Taxes

The February 21, 2025 White House memorandum is the most significant expansion of Section 301 tariffs since the China investigation began in 2017. It signals that the executive branch now treats Section 301 as a general purpose mechanism for protecting American companies from any foreign government policy that systematically extracts value from U.S. businesses not just a remedy for goods-based trade disputes with China. For tech founders and SaaS companies with international revenue exposure, this directive changes the compliance landscape in ways that are only beginning to become visible.

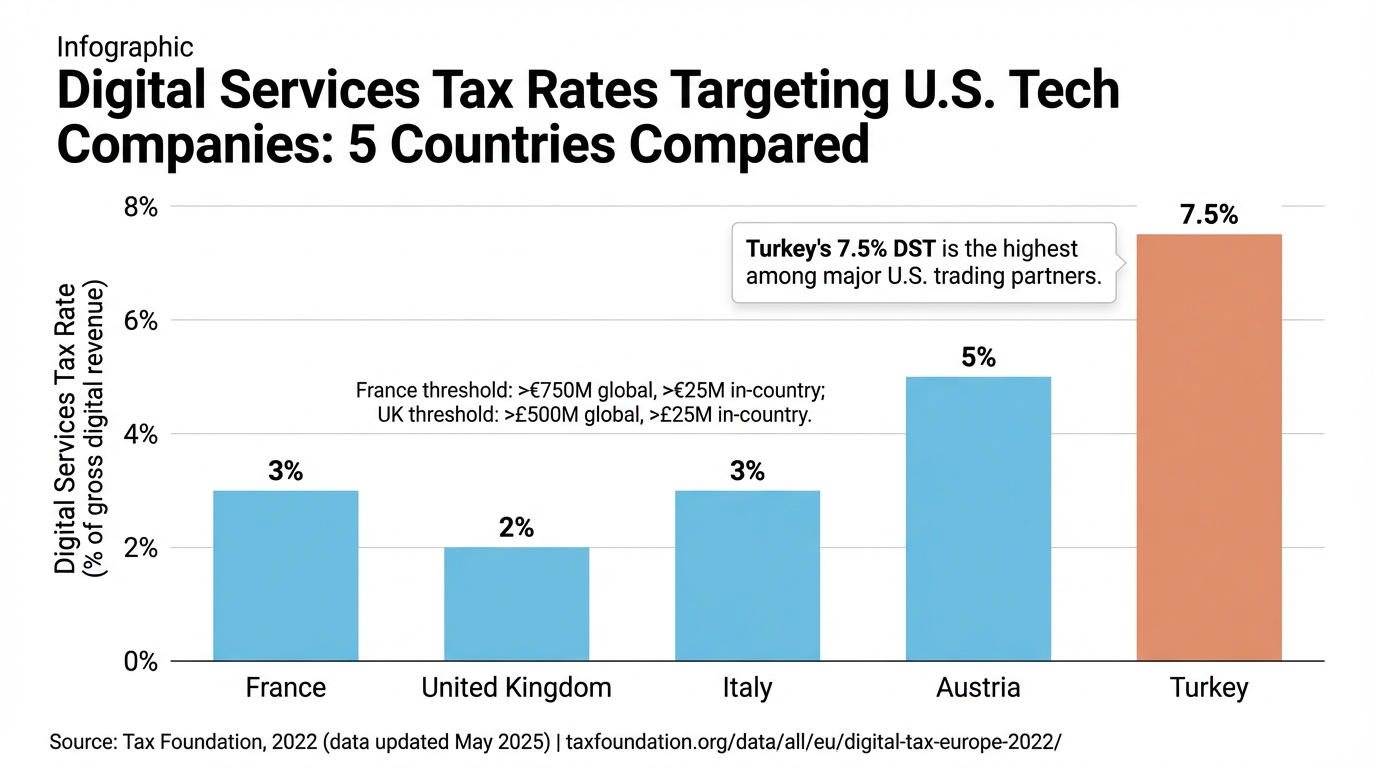

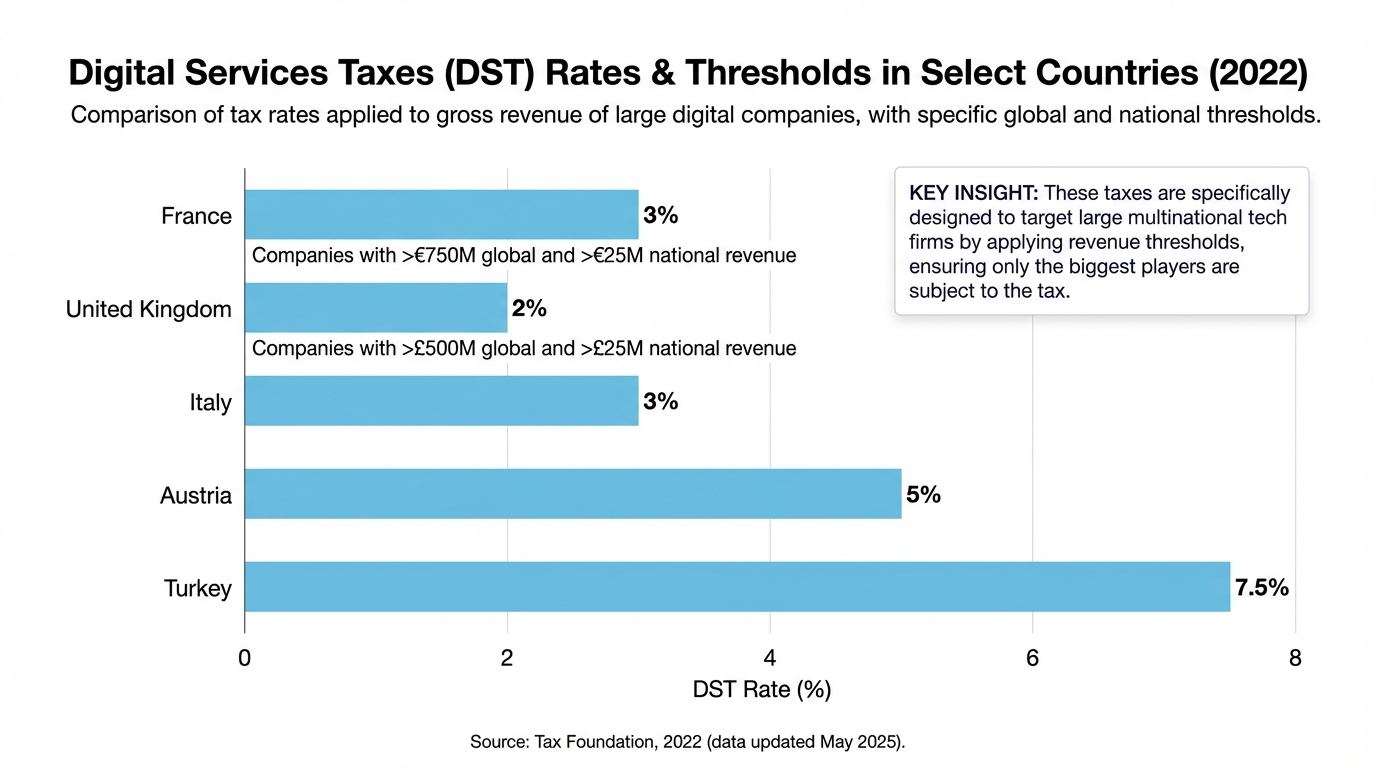

Digital Services Tax Rates Targeting U.S. Tech Companies: 5 Countries Compared Source: Tax Foundation, 2022 (data updated May 2025)

Digital Services Tax Rates Targeting U.S. Tech Companies: 5 Countries Compared Source: Tax Foundation, 2022 (data updated May 2025)

The digital services tax rates that the U.S. government is contesting range from France's 3% to Turkey's 7.5%, and the five countries shown in the chart above illustrate the scope of the DST challenge facing American tech companies in European markets alone.

What the February 2025 White House Memorandum Actually Says and What It Directs the USTR to Do

The February 21, 2025 presidential memorandum, titled "Defending American Companies and Innovators From Overseas Extortion and Unfair Fines and Penalties," is notable for both its policy direction and its rhetorical framing. The document states explicitly that "the gross domestic product of the United States' digital economy alone, driven by cutting-edge American technology companies, has been bigger than the entire economy of Australia, Canada, or most members of the European Union." It then characterizes foreign DSTs as taxes "designed to plunder American companies" and notes that they "could cost American companies billions of dollars."

The memorandum directs the USTR to determine whether to initiate or renew Section 301 investigations into DSTs and other discriminatory foreign practices. The statutory authority cited is 19 U.S.C. § 2411 — Section 301 of the Trade Act of 1974, or what practitioners commonly reference as the section 301 trade act 1974. The scope of practices covered includes: foreign taxes or regulations that discriminate against U.S. digital companies; measures that inhibit their growth; actions that jeopardize their intellectual property; and policies that undermine their competitive position. The memorandum commits the administration to imposing Section 301 tariffs and "other responsive actions" against governments whose tax or regulatory structures impose discriminatory or disproportionate burdens that transfer funds or IP from American companies to foreign entities.

The significance of this directive is the explicit connection between section 301 tariffs and IP protection in the digital services context. The earlier China Section 301 action targeted IP theft and forced technology transfer in the manufacturing and technology sector. The 2025 directive extends the same logic to foreign governments that use tax and regulatory architecture to extract value from American companies' digital IP including their platforms, data systems, algorithms, and digital distribution networks. For the first time, the White House is formally treating discriminatory digital taxation as equivalent to the forced technology transfer that justified the China tariffs.

The USTR is directed to respond within a framework that mirrors the China investigation: Federal Register notices, public comment periods, public hearings, and formal determinations. This creates a timeline and a procedural window. Tech companies whose markets include DST-affected countries should monitor USTR proceedings closely and consider submitting public comments documenting their specific economic exposure.

What Digital Services Taxes Are and Why the U.S. Government Treats Them as Unfair Trade Practices

Digital Services Taxes are levies imposed by foreign governments on revenues generated by large digital businesses operating in their jurisdictions. Unlike conventional corporate taxes that apply based on profit and residency, DSTs typically apply to gross revenue from digital advertising, online marketplaces, data transmission services, and cloud computing. That structural choice, gross revenue rather than profit, is central to the U.S. government's objection.

According to the Tax Foundation, France's DST applies at 3% to companies with over €750 million in global digital revenues and €25 million in French digital revenues. The United Kingdom's Digital Services Tax applies at 2% to companies with over £500 million in global revenues and £25 million in UK revenues. Italy applies 3%, Austria 5%, and Turkey 7.5% with each country's threshold structure designed in a way that captures primarily U.S. technology platforms. The rate spread from 2% to 7.5% across these five countries alone represents substantial variation in the burden on American companies operating across European markets.

According to the Tax Foundation, France's DST applies at 3% to companies with over €750 million in global digital revenues and €25 million in French digital revenues. The United Kingdom's Digital Services Tax applies at 2% to companies with over £500 million in global revenues and £25 million in UK revenues. Italy applies 3%, Austria 5%, and Turkey 7.5% with each country's threshold structure designed in a way that captures primarily U.S. technology platforms. The rate spread from 2% to 7.5% across these five countries alone represents substantial variation in the burden on American companies operating across European markets.

The USTR's objection to DSTs rests on three structural grounds. First, the revenue thresholds in most DST regimes are set at levels that primarily U.S. companies exceed European and Asian digital companies with smaller global revenue bases fall below the threshold and are therefore not taxed. Second, applying the tax to gross revenue rather than profit means profitable and margin-challenged companies alike pay the same rate which is a structure that penalizes companies for scale rather than profitability. Third, the DST base is defined to capture specifically American business models: digital advertising (Google, Meta), online marketplaces (Amazon), and streaming services (Netflix, Apple).

According to the Congressional Research Service, the Trump and Biden administrations both previously challenged DSTs using Section 301 tariffs investigations. The 2019 to 2020 USTR investigations found that DSTs by France, the UK, Italy, Spain, Austria, India, and Turkey "discriminated against U.S. firms" and burdened U.S. commerce. In response, the U.S. announced 25% tariffs on approximately $3.4 billion of those countries' exports but suspended those tariffs pending OECD global tax negotiations. When the U.S. withdrew from the OECD Pillar One framework in 2025, the suspension became unsustainable, and the 2025 memorandum effectively revived the suspended investigations with a more aggressive mandate.

For SaaS founders and digital platform companies, the DST landscape creates a specific IP structuring problem. Revenue recognized in France, the UK, Italy, or Turkey may be subject to gross-revenue taxation regardless of whether the company's underlying IP is located in those jurisdictions. Licensing structures, revenue allocation between jurisdictions, and the location of IP-owning entities all become strategically significant in a DST environment and those structures need to be designed before the USTR makes its determinations, not in response to them. The SaaS Agreement Checklist is a useful starting point for reviewing whether existing licensing and revenue structures are aligned with the current tariff and DST environment.

The Expansion to 16 Countries and What the October 2025 Section 301 Investigation Signals

The October 2025 USTR announcement of Section 301 investigations into 16 trading partners represented the most significant structural shift in the statute's application since the 2018 China investigation. According to AP News, the 16-country scope includes China, India, Japan, the European Union and certain EU member states, the United Kingdom, South Korea, and Mexico, among others. The investigations examine digital trade barriers, discriminatory regulations, excessive subsidies, labor-related trade distortions including concerns about forced labor in manufacturing supply chains and IP-related practices.

The scope of the 16-country investigation is not uniform. Each country faces scrutiny for the specific practices that burden U.S. commerce in that market and China for forced technology transfer and state-directed IP acquisition, EU member states for DSTs and digital regulation that discriminates against U.S. platforms, India for data localization requirements that restrict U.S. digital services companies. These section investigations each follow the same statutory framework despite targeting different foreign government conduct. What unifies the 16-country action is the legal framework: all investigations are conducted under the Section 301 trade act 1974, using the same "unreasonable or discriminatory" standard applied to China since 2017.

Trade analysts quoted by AP News described the expansion as a "bombshell" in U.S. trade policy because it signals that Section 301 tariffs are now a globally deployable mechanism rather than a China-specific response. USTR Ambassador Jamieson Greer stated that the section investigation into each country's practices would examine conduct that suppresses workers' wages and harms American companies including language that suggests the investigations extend beyond IP and DST issues to broader economic competition concerns, including the role of forced labor in creating artificial cost advantages for foreign competitors.

Each of the 16 investigations follows the statutory process: Federal Register notice, public comment period, public hearings, and USTR determination. The procedural timeline means that companies with exposure in multiple markets are facing simultaneous compliance events across different jurisdictions. A compliance team that focused exclusively on China Section 301 tariffs exposure for the past six years now needs to audit global market positions across all 16 investigated countries to understand where new tariff exposure may materialize.

The practical implication for U.S. technology companies is significant: Section 301 tariffs are no longer a China-specific risk factor to be managed through supply chain diversification. They are now a global trade policy instrument that may affect market access, revenue recognition, and IP licensing structures in virtually every major U.S. trading partner.

Section 301 Tariff Lists, Rates, and Affected Products: What Is Actually Subject to Tariffs Today

The practical question for any company importing from China or operating across the markets under USTR investigation is not what Section 301 does in the abstract it is whether specific products, components, or supply chain inputs are covered, at what rates, and how to determine exposure efficiently. This section provides the operational framework.

The Four China Tariff Lists and What Product Categories Each Covers

The China Section 301 tariffs were imposed in four tranches between July 2018 and September 2019, each defined by Harmonized Tariff Schedule (HTS) codes. The structure matters because tariff applicability is determined at the HTS code level, a 10-digit product classification number that determines both standard duty rates and any applicable Section 301 tariffs.

List 1, effective July 6, 2018, covered $34 billion in imports at 25% tariffs. The product selection was deliberate: List 1 targeted industrial machinery, machine tools, aerospace parts, and technology components specifically identified in the USTR's 2018 report as key sectors in China's "Made in China 2025" industrial policy. The goal was to impose costs on the sectors where forced technology transfer china was most systematically occurring.

List 2, effective August 23, 2018, added $16 billion in imports at 25% tariffs, including semiconductors, plastics, chemicals, and railroad equipment. List 3, effective September 24, 2018, was the most expansive covering approximately $200 billion in imports at an initial 10% tariff subsequently raised to 25% in May 2019. According to the Congressional Research Service, List 3 broadened the scope dramatically to include consumer electronics components, networking equipment, furniture, and hundreds of other categories. List 4A, effective September 1, 2019, added $120 billion in imports at 7.5%, including consumer technology products. List 4B was scheduled but tariffs were suspended under the Phase One trade deal negotiated in January 2020.

The combined effect is that approximately $370 billion in Chinese imports, the substantial majority of China's exports to the United States, are now subject to Section 301 tariffs at rates ranging from 7.5% to 25% on top of standard MFN duty rates. Determining whether a specific product is covered requires starting with the 10-digit HTS code and cross-referencing it against the USTR's Section 301 tariff list database, which is maintained at USTR.gov and searchable by code.

Understanding how to read and interpret IP claims is equally important in this context, because patent claims define the technical boundaries of what is protected and knowing whether a Chinese-sourced component potentially infringes a U.S. patent is a related compliance question that arises alongside tariff classification.

The 2024 Tariff Rate Increases and Which Technology Sectors Face the Steepest New Burdens

The September 2024 four-year review produced targeted increases in strategic sectors, applied on a phased schedule extending through 2026. According to AP News, electric vehicle tariffs rose from 25% to 100% bringing total duty on Chinese EVs to 102.5% when combined with standard MFN rates. Solar cell tariffs increased from 25% to 50%. Semiconductor tariffs were set to reach 50% by 2025. Lithium-ion EV battery tariffs rose from 7.5% toward 25% on a phased schedule. Ship-to-shore cranes, medical gloves, syringes, and needles also saw substantial increases.

The pattern is consistent across all targeted sectors: they are industries where China has used IP acquisition including through forced technology transfer and, in some manufacturing supply chains, through forced labor and state subsidy to build structural overcapacity that undercuts domestic U.S. production. The USTR's 2024 determination linked the rate increases explicitly to China's continued failure to reform the practices documented in the 2018 investigation.

For technology founders and product companies, the semiconductor and electronics component increases carry the most immediate supply chain significance. Semiconductor section 301 tariffs at 50% affect hardware components, IoT devices, embedded systems, and the electronics in virtually every technology product that has any China-sourced component in its bill of materials. Companies that modeled their cost structures at the original 25% rate need to recalculate with the 2025 rate in effect and with the possibility of further increases at the next review cycle. For SaaS and software companies, protecting the software itself through patents and other IP mechanisms remains a parallel and equally urgent priority alongside tariff compliance.

The 2024 increases also demonstrated something important about how the four-year review works in practice: the USTR does not simply maintain or terminate section tariffs as it can increase them significantly when the evidence supports doing so. Companies should treat each four-year review as a material business event requiring advance analysis of potential rate changes, not a routine administrative checkpoint.

The Exclusion Process and How to Request Relief From Section 301 Tariffs

Section 301 tariffs are not absolute. The USTR has maintained an exclusion process that allows importers to petition for product-specific relief when the tariff creates severe economic harm, when the product is genuinely unavailable from non-Chinese sources, or when the tariff would undermine rather than support domestic production objectives.

The exclusion process has operated in multiple phases, and the new exclusion process for each list round has followed a similar structure. Initial exclusion rounds opened in 2019 and 2020 for Lists 1, 2, and 3, with subsequent rounds for List 4A. Each exclusion is product-specific and defined by HTS code and a detailed product description and time-limited, typically to one year, subject to renewal through a separate process. The USTR administers the process through an online portal, and petitions require detailed factual support: documentation that the product is not reasonably available from domestic or non-Chinese sources, evidence that the tariff causes severe economic harm disproportionate to its trade policy benefit, and a statement of the national economic interest basis for granting relief.

A granted exclusion has retroactive effect to the date of petition filing, meaning that if a company has been paying section 301 tariffs on a product for which an exclusion is subsequently granted, it is eligible for refund of duties paid during the pendency of the petition. For products with significant import volume, that retroactive refund can be substantial. The process is competitive and not all petitions are granted, but companies currently paying Section 301 tariffs on products with no viable non-Chinese supply alternative should evaluate whether an active exclusion opportunity exists or whether a new petition round has been opened by the USTR.

How Section 301 Tariffs Interact With the International Emergency Economic Powers Act and Current Legal Challenges

The Section 301 tariff regime does not operate in isolation. Since 2025, it has been stacked with a parallel tariff regime imposed under the International Emergency Economic Powers Act (IEEPA), a different statutory authority with different procedural requirements and different legal vulnerabilities. Understanding how these two regimes interact is essential for calculating actual duty exposure and for assessing the legal stability of the tariff environment.

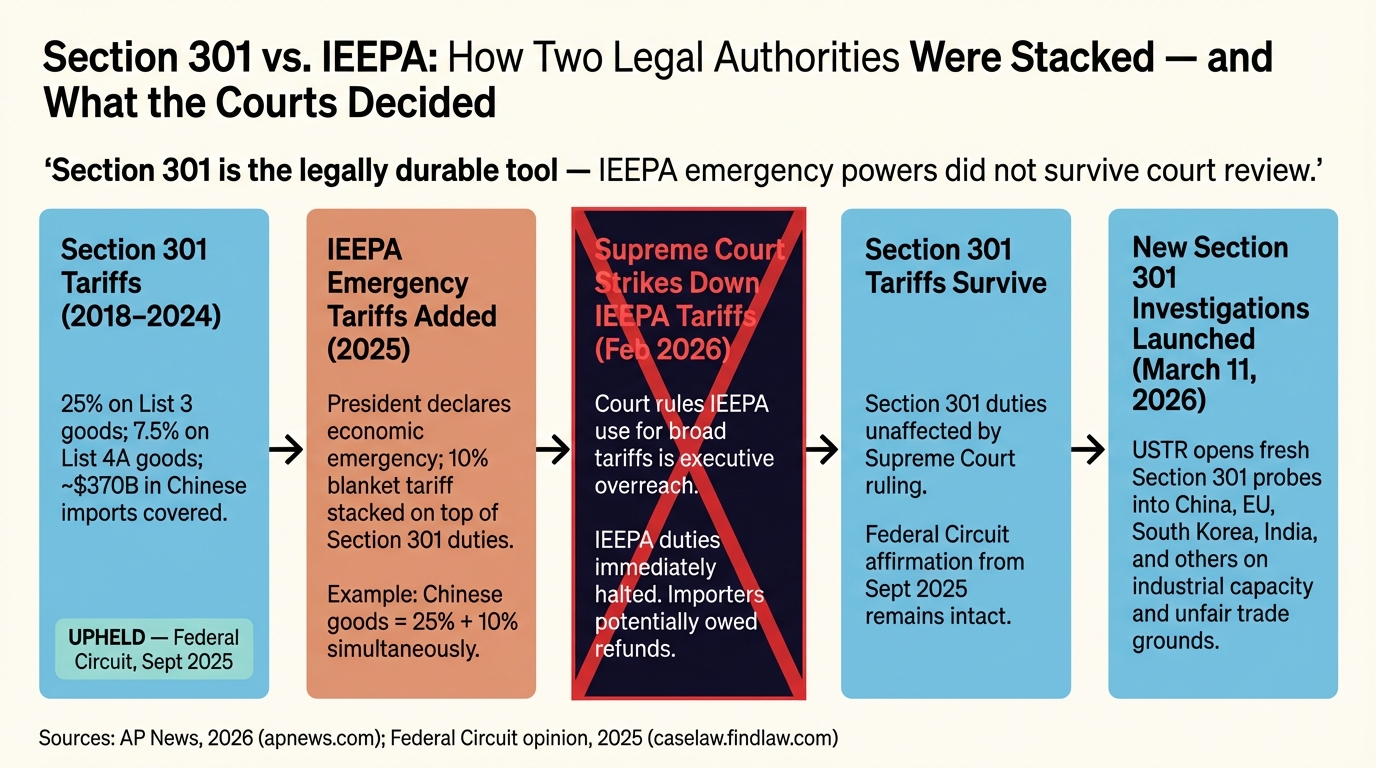

Section 301 vs. IEEPA: How Two Different Legal Authorities Were Stacked and What the Courts Decided Source: AP News, 2026; Federal Circuit opinion, 2025

Section 301 vs. IEEPA: How Two Different Legal Authorities Were Stacked and What the Courts Decided Source: AP News, 2026; Federal Circuit opinion, 2025

The process chart above illustrates how the two authorities were stacked and what the courts have determined about each regime's legal validity.

What IEEPA Tariffs Are and Why the Trump Administration Used Both IEEPA and Section 301 Simultaneously

The International Emergency Economic Powers Act, codified at 50 U.S.C. § 1701 et seq., grants the President broad economic powers during declared national emergencies. Unlike Section 301 of the trade act of 1974, IEEPA does not require an investigation, a Federal Register notice and comment period, or a finding of specific unfair trade practices as it requires a national emergency declaration. The Trump administration's 2025 IEEPA tariff program imposed a 10% universal baseline tariff on imports from most countries and country-specific "reciprocal" tariffs at higher rates.

For Chinese imports specifically, the tariff stacking effect became extreme: goods from China became subject to Section 301 tariffs (25% on most categories), plus IEEPA tariffs that reached 145% on Chinese goods as announced in April 2025, plus standard MFN duty rates. The cumulative effect made the landed cost of many Chinese-sourced components economically nonviable regardless of the underlying product or supply chain relationship.

The Trump administration chose to use both IEEPA and section 301 tariffs simultaneously for complementary reasons. Section 301 tariffs rest on a well-developed factual and legal record, seven years of investigation findings, four-year reviews, litigation that has established their validity through the Court of International Trade and the Federal Circuit. IEEPA tariffs are faster but procedurally thinner as they rely on an emergency declaration rather than an investigation record. Using both creates redundancy: if IEEPA tariffs are successfully challenged in court, section 301 tariffs remain in place, and vice versa.

For importers, the stacking calculation is the essential starting point for supply chain decisions. A company sourcing a hardware component from China at $100 might face a 25% section 301 tariff ($25), a 145% IEEPA tariff ($145), and a standard MFN duty of 3 to 5% ($3 to $5), producing a total landed cost of $273 to $275 for a $100 component. At those levels, even significant logistical cost premiums for non-Chinese sourcing become economically attractive.

The Legal Challenges to Section 301 and IEEPA Tariffs and Where They Currently Stand

Section 301 tariffs have faced sustained legal challenges since 2019. The most significant, HMTX Industries LLC v. United States, argued that the USTR exceeded its statutory authority in applying tariffs to List 3 goods without proper procedural compliance. The Court of International Trade ruled against the tariffs on procedural grounds in 2021, but the Federal Circuit reversed, upholding the USTR's statutory authority. The Supreme Court declined to hear the case, leaving the Section 301 tariffs in place and establishing that they rest on solid legal footing through the current appellate review hierarchy.

The 2025 IEEPA tariffs have generated a separate wave of legal challenges, with plaintiffs arguing that IEEPA does not authorize broad tariff imposition of this scale and that the statute was designed for targeted financial sanctions in genuine national security emergencies, not for general trade policy. Those challenges have been working through the Court of International Trade, and the legal questions, including any potential Supreme Court IEEPA ruling, turn on whether the President's emergency declaration satisfies the statutory threshold and whether tariffs fall within IEEPA's authorized economic measures.

According to Duane Morris, as of April 2026, the IEEPA legal challenges have generated significant litigation activity, with multiple cases in active briefing. The legal distinction between section 301 tariffs and IEEPA tariffs matters for compliance planning because section 301 tariffs have a much stronger legal foundation and they have survived multiple rounds of litigation while IEEPA tariffs face genuine legal uncertainty. Companies making long-term supply chain decisions should not assume IEEPA tariffs will survive judicial review in their current form, but they should also not assume they will be eliminated quickly.

For U.S. technology companies, the most practically significant implication of the legal landscape is that Section 301 tariffs are durable and should be treated as a permanent feature of the U.S. – China trade relationship for planning purposes, carrying significant compliance obligations that require ongoing monitoring. IEEPA tariffs are more volatile as they may be modified, suspended, or invalidated and supply chain decisions based on IEEPA rates alone carry regulatory risk that Section 301-based decisions do not.

What Section 301 Means for U.S. Technology Companies and Their IP Strategy

The Section 301 tariff regime is not only a trade policy instrument, it is a statement about the value of American intellectual property and the government's willingness to use economic leverage to protect it. For technology founders, SaaS companies, and innovators whose IP is their primary asset, the practical implications of section 301 tariffs extend well beyond import duty compliance.

How Section 301 Investigations Create IP Strategy Obligations for Tech Companies

When the USTR initiates or renews a Section 301 investigation, whether targeting China's forced technology transfer practices or a foreign government's Digital Services Tax, it opens a public comment period that directly affects the investigation's scope and the ultimate tariff determination. Technology companies with exposure to the practices under investigation have both a right and a strategic interest in participating.

In the forced technology transfer china context, U.S. companies that have experienced IP extraction, been pressured to enter joint ventures on non-commercial terms, faced below-market licensing demands from Chinese partners, or had proprietary technology accessed without authorization by Chinese government entities or state-backed firms have relevant evidence to contribute. The USTR's investigation record is strengthened by specific, documented examples and companies that contribute such documentation are better positioned to have their specific market access and IP concerns addressed in the resulting tariff determinations.

In the DST context, SaaS companies and digital platform businesses that pay DSTs in France, the UK, Italy, Turkey, Austria, or other covered jurisdictions should calculate their actual DST burden and assess whether to submit that data through the public comment process. The USTR's quantification of the harm to U.S. commerce, the factual predicate for any tariff action, is built partly from industry submissions.

IP strategy in the Section 301 tariffs era also requires attention to licensing structure. If your company licenses IP to subsidiaries or third parties in DST-affected jurisdictions, the location of the IP-owning entity, the royalty terms, and the characterization of the revenue stream all affect DST exposure. These structures should be reviewed in light of the USTR's active investigations, because the DST that a foreign government imposes on your gross revenue in their jurisdiction is exactly the type of discriminatory extraction the 2025 White House memorandum identified as a target for Section 301 action. Founders who have not yet secured comprehensive patent protection for their core innovations should review common patent filing mistakes before entering any China-adjacent commercial arrangement.

Forced Technology Transfer Risk Assessment for Founders Considering China Market Exposure

The USTR's 2018 investigation documented that the risk is not speculative. China's regulatory framework creates multiple channels through which proprietary technology can be transferred without the consent or adequate compensation of the foreign IP owner. Those channels include mandatory joint venture structures, administrative licensing requirements that demand trade secret disclosure, state-directed acquisition programs, and in some sectors, the involvement of forced labor in manufacturing operations that benefit from the acquired technology. The IP Commission Report estimated annual losses to U.S. companies from Chinese IP theft at between $225 billion and $600 billion which is a figure that reflects the aggregate cost of a systemic policy, not isolated incidents.

A practical pre-entry IP risk framework for China market engagement should address at least four questions. First, which specific IP assets would need to be disclosed to any Chinese partner, government entity, or regulatory body as a precondition for market access and are those assets core to the company's competitive advantage or peripheral? Second, can the relevant commercial objective be achieved through a structure that minimizes IP disclosure which is a distribution agreement rather than a technology license or a services arrangement rather than a joint venture? Third, has the company conducted a freedom-to-operate analysis for Chinese patent filings in its technology category because Chinese domestic companies and state-owned enterprises have filed extensive patent portfolios in strategic sectors, and market entry may require navigating a Chinese patent landscape that looks very different from the U.S. or European landscape? Fourth, are the trade secret protections that the company relies on in the U.S. context enforceable against Chinese counterparties in Chinese courts, or does the enforcement mechanism depend on the same state infrastructure that may facilitate the transfer?

Before sharing any proprietary information with a potential Chinese partner or regulatory body, a Patent Non-Disclosure Agreement provides a foundational layer of contractual protection, though founders must understand that contractual protections alone are insufficient against state-directed forced technology transfer china mechanisms and should be combined with structural IP safeguards.

The Section 301 tariff regime provides U.S.-level economic consequences for Chinese government behavior but it does not recover IP that has already been transferred. The pre-entry framework is the primary protection mechanism for founders. Section 301 tariffs are the macro-economic backstop, not the company-level shield.

Patent Strategy as a Complement to Section 301 Protection

Section 301 tariffs impose economic costs on China at the national level, but individual technology companies need company-level IP protection that operates regardless of the tariff environment. Patents are the most durable form of that protection, and the China Section 301 tariffs context makes patent strategy more important for U.S. technology companies.

When the U.S. government determines that a sector is subject to forced technology transfer China risk as it did in the 2018 USTR investigation and that sector's companies should ensure their core innovations are protected by patents in the relevant jurisdictions. A patent provides a legally enforceable right to exclude others from practicing the claimed invention, including in markets where trade secret protection may be inadequate. In China, where trade secret enforcement through Chinese courts is compromised by the state involvement in technology acquisition that Section 301 tariffs were designed to address, patent protection provides a more robust legal baseline.

PCT international patent applications allow a single filing to establish priority in over 150 countries, including China, and are strategically important for technology companies with global market ambitions or global competitor exposure. A PCT application filed within 12 months of the U.S. priority date preserves the right to enter national phase in China and other major markets giving the company a patent right in the market where the technology is most at risk of being appropriated.

For SaaS founders and AI technology companies specifically, software and AI patent strategy in the Section 301 tariffs era requires attention to both the U.S. and Chinese patent landscapes. China has become an extremely active patent jurisdiction for AI, machine learning, and software-related inventions as Chinese domestic companies and state-backed research institutions file hundreds of thousands of technology patents annually. The AI patent opportunity for U.S. companies is real, but it requires proactive filing strategy before entering any China-adjacent commercial relationship. A U.S. company entering any such relationship without understanding the Chinese patent landscape in its technology category is taking on risk that can be assessed and mitigated with appropriate prior art searches and freedom-to-operate analysis. Reviewing recent software patent examples from leading technology companies can help founders understand the scope of protection that is achievable and the claim structures that hold up best in contested markets.

The connection between Section 301 tariffs and patent strategy is not incidental: the 2018 USTR investigation found that China's forced technology transfer practices were most concentrated in the same sectors such as semiconductors, AI, robotics, aerospace, and advanced manufacturing where Chinese industrial policy most aggressively targets foreign IP for acquisition. A robust patent portfolio in those sectors is both commercial insurance and a component of the national-level IP protection strategy that Section 301 tariffs are intended to support. The Patent Analysis Playbook outlines how to use competitive IP data to identify where your technology is most exposed and how to build a portfolio that addresses those vulnerabilities systematically.

Frequently Asked Questions About Section 301 Tariffs

What is the difference between Section 301 and 232 tariffs?

Section 301 of the Trade Act of 1974 and Section 232 of the Trade Expansion Act of 1962 are both U.S. trade remedy statutes, but they operate under entirely different legal frameworks and target different types of problems. Section 232 authorizes tariffs when the President, based on a Department of Commerce investigation and a Department of Defense national security finding, determines that imports threaten national security. The 2018 steel (25%) and aluminum (10%) tariffs imposed under Section 232 are the most prominent recent examples. Section 301 authorizes tariffs when the USTR determines that a foreign government's practices are "unreasonable," "unjustifiable," or "discriminatory" and burden U.S. commerce as no national security finding is required. Section 301 tariffs target foreign government behavior; Section 232 tariffs target import levels that threaten national security. The China tariffs of 25% on most goods are Section 301 tariffs; the steel and aluminum tariffs are Section 232. Both can be stacked with each other and with IEEPA tariffs, which is why total duty burdens on some Chinese imports now exceed 150%.

Does Section 301 only apply to China?

No — Section 301 of the Trade Act of 1974 is a general statutory authority that applies to any foreign government whose practices the USTR determines are "unreasonable," "unjustifiable," or "discriminatory" and burden U.S. commerce. The China section 301 tariffs action that began in 2018 is the largest and most consequential in the statute's history, but it is not the only one. The USTR has used the Section 301 trade act 1974 against the European Union (over Airbus subsidies), France (over its Digital Services Tax), and in 2019 and 2020 against France, the UK, Italy, Spain, Austria, India, and Turkey for their DSTs. The October 2025 expansion to 16 trading partners, including EU member states, Japan, South Korea, India, and Mexico, demonstrates that Section 301 tariffs are now being deployed as a globally applicable mechanism. Any foreign government practice that meets the statutory threshold is potentially subject to Section 301 investigation and tariff consequences.

What is Section 301 of the US Trade Act?

Section 301 of the Trade Act of 1974 (19 U.S.C. § 2411) is the primary U.S. statute authorizing the government to respond to foreign government practices that harm American businesses and restrict U.S. commerce. It grants the United States Trade Representative authority to investigate those practices, negotiate with the foreign government to eliminate them, and impose tariffs or other economic measures if the foreign government refuses to change. Unlike most trade remedy statutes, the section 301 trade act 1974 does not require proof of injury through a formal determination, rather the USTR needs only to find that the foreign practice is "unreasonable," "discriminatory," or "unjustifiable." The statute covers a broad range of foreign government behavior, from conventional tariff barriers to regulatory discrimination, forced technology transfer, and digital services taxes. It was originally enacted as part of the Trade Act of 1974, signed into law as Public Law 93-618.

What is Section 301 in the US?

Section 301 refers to Section 301 of the Trade Act of 1974, codified at 19 U.S.C. § 2411, which is one of the most powerful trade remedy tools available to the U.S. government. When the USTR determines that a foreign government is engaging in practices that are "unreasonable" or "discriminatory" and burden U.S. commerce, Section 301 authorizes a range of responsive actions including tariffs, import restrictions, and other economic measures. In common usage, "section 301 tariffs" refers most frequently to the tariffs imposed on approximately $370 billion in Chinese imports beginning in 2018, following a USTR investigation that documented China's systematic forced technology transfer and IP theft. The February 2025 White House memorandum expanded the statute's application to digital services taxes and other foreign measures targeting U.S. technology companies, extending Section 301 tariffs from manufactured goods to the digital economy.

How does forced labor factor into the Section 301 and broader trade enforcement framework?

Forced labor in Chinese manufacturing supply chains is a distinct but related trade enforcement concern. The Uyghur Forced Labor Prevention Act (UFLPA), enacted in 2021 as the key forced labor prevention act for supply chain compliance, creates a rebuttable presumption that goods manufactured in Xinjiang or by entities on the UFLPA Entity List were produced using forced labor and are therefore prohibited from importation under 19 U.S.C. § 1307. This statute operates separately from section 301 tariffs but addresses overlapping conduct: the same state-directed economic system that facilitates forced technology transfer china also deploys forced labor as a structural cost advantage in manufacturing. U.S. Customs and Border Protection enforces forced labor import prohibitions at the border independently of the Section 301 tariff regime. Companies sourcing from China should conduct global supply chain due diligence practices for forced labor compliance in addition to Section 301 tariff classification with both compliance obligations apply simultaneously and carry independent penalties for non-compliance.

Your Next Steps to Section 301 Tariffs Success

Section 301 tariffs are no longer a background policy detail for technology companies as they are a first-order business variable affecting supply chain costs, IP licensing structures, market access strategy, and competitive positioning across virtually every major trading relationship the U.S. maintains.

The Section 301 trade act 1974 framework has now been applied to cover approximately $370 billion in Chinese imports, is actively expanding to 16 additional trading partners, and has been explicitly extended by the 2025 White House memorandum to protect American IP from foreign digital taxation. For technology founders, SaaS companies, and IP-intensive businesses, the window for proactive positioning is now before USTR determinations lock in new tariff structures and before China market engagements expose proprietary technology to a forced technology transfer system that has cost U.S. companies an estimated $225 billion to $600 billion annually.

The bottom line: A passive approach to Section 301 tariffs (i.e., waiting to see what the USTR determines and reacting afterward), leaves technology companies exposed to tariff rate increases they did not model, IP extraction they cannot reverse, and DST burdens they cannot recover. A proactive approach means auditing tariff exposure across all China-sourced inputs at current stacked rates, reviewing IP licensing structures in DST-affected jurisdictions, filing PCT applications to establish patent priority in markets where forced technology transfer risk is highest, and participating in USTR public comment periods when the practices under investigation affect your business.

The urgency is not hypothetical. The four-year review cycle will continue to generate potential rate increases. The 16-country Section 301 investigations are proceeding through the statutory process now. And any technology founder who shares proprietary IP with a Chinese partner before implementing appropriate structural protections may find that the macro-level shield provided by section 301 tariffs does not recover the specific IP that was transferred.

To protect your position:

- Schedule a Free IP Strategy Call with Andrew Rapacke at Rapacke Law Group to assess your section 301 tariff exposure, IP protection gaps, and PCT filing priorities

- Audit every China-sourced component in your bill of materials against current section 301 tariffs rates of 25% on most goods, 50% on semiconductors as of 2025

- Review existing licensing agreements and IP ownership structures for DST exposure in France, the UK, Italy, Turkey, and Austria

- File or update provisional patent applications for any innovations that may be disclosed in China-adjacent commercial arrangements

- Monitor USTR Federal Register notices for public comment periods on all 16-country Section 301 investigations and submit comments documenting your specific economic exposure

- Conduct a freedom-to-operate analysis in the Chinese patent landscape before entering any market engagement that involves technology disclosure

Rapacke Law Group's fixed-fee patent and IP strategy services mean you will know the cost of protecting your IP before you commit. There are no billable hour surprises and no ambiguity about what the engagement entails. The firm offers a full refund if a patentability search finds your invention is not novel because the firm's interest is in protecting IP that is worth protecting, not in the “nickel and dime” billable hour model.

To Your Success,Andrew Rapacke is Managing Partner and Registered Patent Attorney at Rapacke Law Group, where he advises technology founders, SaaS companies, and innovators on patent prosecution, IP portfolio strategy, and international IP protection. He is the author of the IP Insights newsletter and creator of the AI Patent Mastery resource for technology founders navigating the evolving AI patent landscape.